Expectations heading into 2026 were for a relatively positive environment, and January and February delivered on this, with solid gains across most asset classes. Global equities continued their strong run, while South African assets remained resilient.

In March, there was a sudden change after US and Israeli attacks on Iran, which led Iran to close the Strait of Hormuz. This strait is an important shipping route where about 20% of the world’s oil passes every day. The closure raised concerns about disruptions to energy supplies and higher oil prices, thereby increasing inflation expectations.

As inflation expectations shifted, expectations for central bank interest rate decisions also changed. Central banks use interest rates to manage inflation and support economic stability. Markets moved from pricing in rate cuts to expecting rates to stay higher for longer or even rise. This triggered a broad repricing across markets and a global move away from riskier assets.

Higher interest rates typically put pressure on asset prices. Equities decline as future earnings are discounted more heavily, bonds and property become less attractive relative to higher available yields, and gold can come under pressure as it does not generate income.

Source: PortfolioMetrix

Global markets

Where a market is located and what it produces largely determine who performed well this quarter.

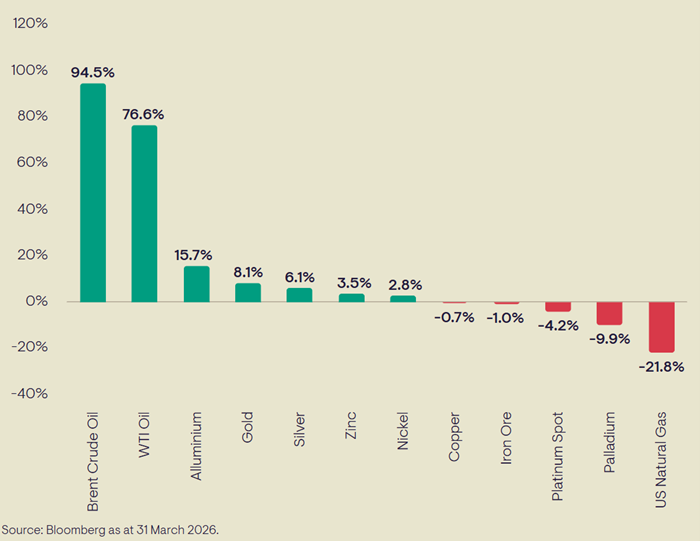

Energy-exporting regions showed strong equity returns. Latin America gained 16.4%, with Brazil rising over 22% as higher oil prices helped commodity exporters. The Pacific region, excluding Japan, returned 3.9%, and Japan returned 1.4%.

These returns were supported by demand for AI-related semiconductors and favourable domestic policies. The UK’s FTSE 100 ended the quarter at 0.8%, impacted by its ties to oil and mining.

Source: Bloomberg

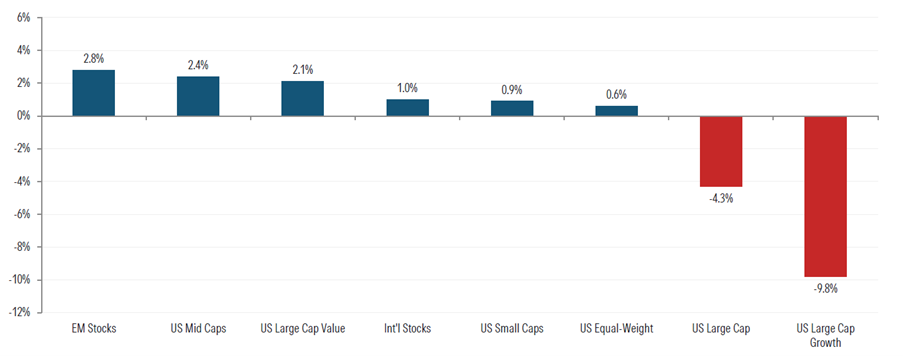

The United States did not perform well in the markets, even though it is the world's largest oil producer. The S&P 500 dropped by 4.3%, and the NASDAQ fell by 5.8%. This happened because US markets are mainly made up of big technology companies instead of energy producers.

When inflation and interest rates increased, the value of these growth-focused companies fell. In a more cautious environment, investors moved their money into the US dollar and government bonds instead of US stocks.

Source: Morningstar as of 10 April 2026.

Global infrastructure performed well, returning 8.3% in USD. This success came from pipelines and energy networks that directly benefited from the rise in oil prices. In contrast, global property had a modest return of 0.5%. Global bonds decreased by 0.8% in USD, which is unusual when stocks are down. However, this decline was driven by inflation concerns, causing yields to rise and prices to drop.

Gold ended the quarter up 7.8%, but this hides significant volatility. In March, it fell sharply, dropping from $5 400 to $4 100 per ounce, its worst weekly decline in over 40 years. Rising interest rates have made income-generating assets more attractive. It recovered somewhat after the ceasefire, but this is a reminder that gold does not always behave as a safe haven.

South Africa: Geopolitics overshadows domestic positives

South Africa entered 2026 with momentum, and this continued through the first two months.

Inflation fell to 3% in February, in line with the Reserve Bank’s target. The budget speech was also better than expected. Tax revenue was higher, deficits were expected to narrow, and debt looked more under control. Markets reflected this improved sentiment.

South Africa is a commodity-based emerging market and a net importer of oil, making it vulnerable when global investors grow cautious and energy prices rise. Money moved out of higher-risk markets, such as South Africa, and into safe havens, such as the US dollar.

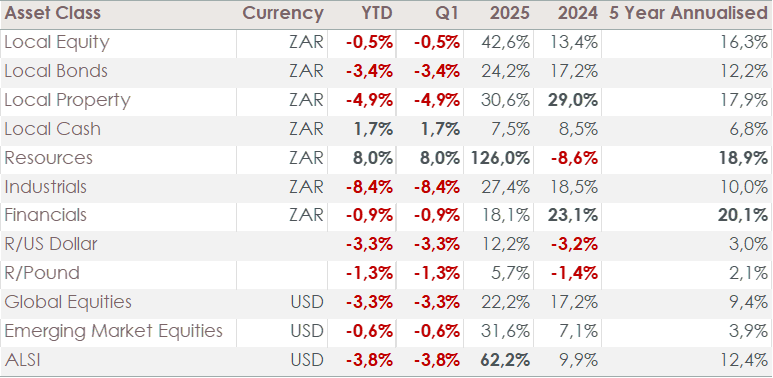

The JSE fell 10.5% in March, leaving it down 0.6% for the quarter. Year to date, the strongest performers have been Sasol (+122%), Glencore (+40.4%), and BHP Group (+22.7%), all within the basic materials sector. In contrast, the biggest detractors were Prosus (-24.9%), Harmony Gold Mining (-24.1%), and Naspers (-22%). At a sector level, technology and consumer discretionary stocks have struggled the most.

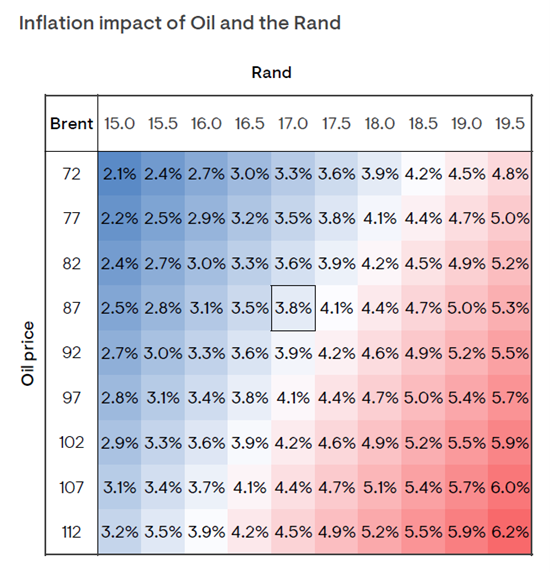

The Rand weakened to R16.94/USD, down 3.3% against the dollar and 1.3% against the pound. The chart below illustrates the relationship between oil prices and currency movements. As oil prices rise, the Rand tends to weaken, and when prices fall, it tends to strengthen. A weaker currency makes imports, including oil, more expensive and adds to inflation pressure.

Source: NinetyOne

To manage this, the South African Reserve Bank took a cautionary stance and decided to keep interest rates at 6.75% at the most recent meeting. The market has shifted from expecting two to three cuts in 2026 to pricing in potential hikes.

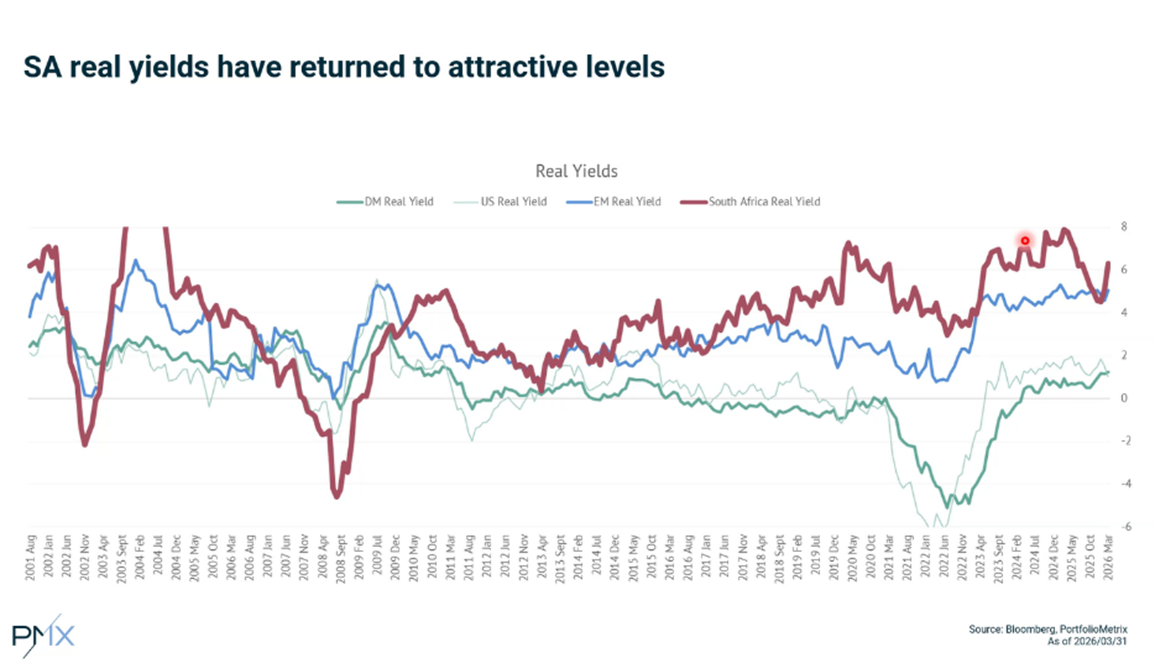

The bond sell-off has pushed South African real yields to more attractive levels.

At these levels, local bonds offer compelling returns relative to developed markets, where real yields are lower. Sustained foreign investment could be a positive, but this will depend on how inflation evolves.

Source: PortfolioMetrix

How did our portfolios perform?

With most asset classes declining over the quarter, portfolios across risk profiles ended slightly negative. Returns ranged from approximately -1% to -2.5% locally, and -1.5% to -4.8% globally in USD terms.

It is important to view this in perspective. Over the past 12 months, returns have remained strong, ranging from 15.3% to 17.8% locally and 13.2% to 18.5% globally in USD terms.

Looking ahead into 2026

Q1 2026 was an unusual “nowhere to hide” quarter, where almost all asset classes delivered negative returns.

A ceasefire was announced in late March, and the strait was tentatively reopened, but the situation remains highly unstable, with access changing frequently as US–Iran tensions evolve.

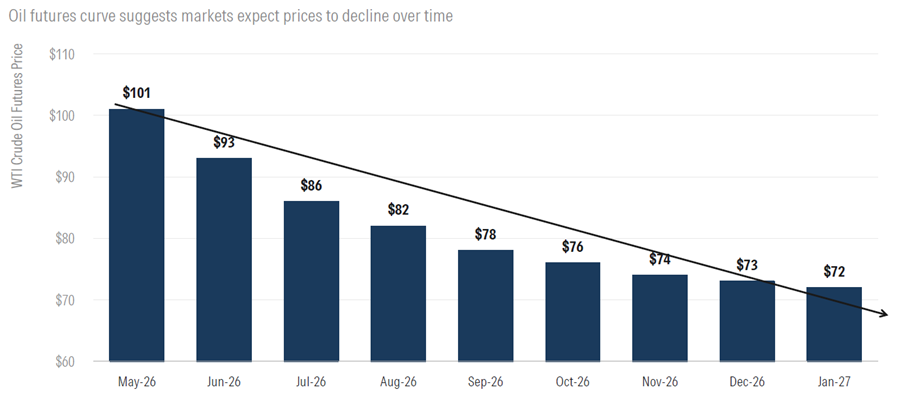

If it remains open on a sustained basis and oil prices ease, inflation should gradually come back under control, and central banks will have room to consider cutting interest rates again in the second half of the year. Oil markets currently suggest prices could fall back towards $72 to $80 per barrel by early 2027, which would be a meaningful relief.

Source: Morningstar

The key risk is that the ceasefire does not hold. If tensions escalate again and oil prices stay high, inflation is likely to remain elevated or rise further. This would keep interest rates higher for longer and continue to weigh on financial markets.

For South Africa, the next few months of inflation data will be important, especially whether higher fuel costs feed through into broader inflation. This will determine whether the Reserve Bank can hold interest rates steady or may need to raise them.

South African equities have recovered well over the past three years, supported by improving conditions and previously attractive valuations. That valuation gap is now largely closed. Going forward, returns are more likely to depend on real economic progress and continued structural reform, but global uncertainty remains a risk. The easy gains have largely been made, but the long-term case for South Africa remains intact.

Market conditions like these can feel unsettling, especially when losses happen quickly and across multiple asset classes.

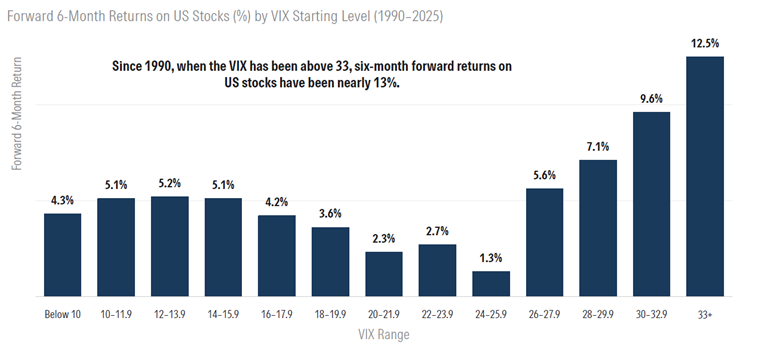

Market declines of around 20% happen every few years, so this situation isn't unusual. Although the drop has been sharp, history shows that similar periods are often followed by strong recoveries. For example, after past declines, US markets have averaged returns of about 13% in the following year.

Source: Morningstar

The key is how one responds. Staying invested in a well-diversified portfolio is essential to navigating short-term uncertainty and benefiting from recovery. Uncertainty and volatility are part of investing, and the portfolios you hold are designed with this in mind.

A disciplined investment process, applied consistently over time, adds value and helps avoid costly decisions in periods like these, whether that means stopping contributions when markets fall or moving to cash and missing the recovery that often follows.

Read the full PortfolioMetrix quarterly local report here, and the full quarterly offshore report here.

<Foundation Family Wealth is an Authorised Financial Services Provider>